Finance, land and lives

Money flows that shape the places we live

A through-thread in my career has been tying local and specific contexts up into the global trends that affect them. Perhaps nowhere does that play out more than in the way finance influences the places we live and work.

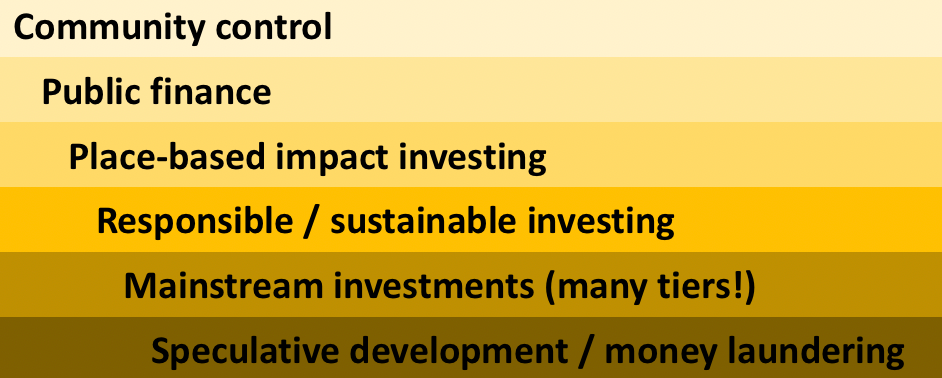

You can see finance in built environments as sitting along a spectrum, illustrated by this simple line:

It’s great to see growing work and awareness on how to engage at various points along that line. All are needed – scaling up strategies on the “proximity and connection” side, and curbing and challenging those on the speculative “distance and extraction” side.

There is a spectrum of types of ownership and investment involved. To simplify (excessively):

Community control

Last year’s winner of the World Habitat Awards was the Brussels Community Land Trust, which develops affordable housing on community-owned land. The homes are bought by people on low incomes, 83% of whom have a migrant background. This World Habitat report shares other powerful examples: from work to establish a favela community land trust in Rio de Janiero, to community housing initiatives in Eastern Europe.

Check out the Center for Community Land Trust Innovation for other global examples and updates.

Community control is not limited to land ownership of course. Every day, in ways big and small, people individually and collectively shape the nature of the places where they live. The extent to which people have the freedom to do this, though, has a lot to do with the economy writ-large, as well as its specific role in determining the nature of their surroundings.

Public ownership and finance

Governments, from local to national, play a key role in determining how finance plays out in places. This includes their regulatory and planning functions of course, with planning being a determining factor in whether narrow financial interests call the shots, or if finance is harnessed to address wider needs.

There’s government as a provider of finance (directly, and as a partner to or facilitator of private finance) – a role that in some countries has expanded significantly in the context of COVID recovery, presenting a key advocacy and leverage opportunity. And there’s government as an owner of public land and places: for which accountability over how that land is used (accessible to whom), and maintained, is key.

Place-based impact investing

Impact investing can be powerful, and is growing fast. But a lot can go wrong when in reality it skews more to the “distance and extraction” side of the line, with impact investors on one side of the world deciding what “impact” means in the lives of people on the other, and expecting unrealistic levels of return on their investments in the process.

A classic example is investments into renewable energy projects that displace communities from their land and/or fail to generate medium or long-term economic opportunities locally comparable to what was there beforehand.

It’s good to see the US Impact Investing Alliance recognize the importance of genuine local participation. Their updated approach recognizes the “need for transparency, accountability and an equitable distribution of power and resources across our economy.” The first of their two priorities is “transforming community investing”, stating that (in the US context):

“for decades, impact investors have leveraged their capital to support positive outcomes like affordable and safe housing, strong entrepreneurial ecosystems and healthy, resilient communities. Building on this history, we must now consider how to better empower community members, through authentic community engagement and cutting-edge practices, such as participatory investments.”

Meanwhile Transform Finance has been working on multiple fronts to support social justice actors in local communities “so that they have the necessary inspiration, knowledge, and strategies to influence how investors deploy their capital”.

Which leads to…

Responsible capital allocation

There’s growing awareness that a check-box approach to “ESG” (environmental, social and governance issues) does little if anything to change the effects of the real world economy in people’s lives.

Systems-level approaches are gaining attention: encouraging asset owners to engage with the risks to people, planet and the economy across the full breadth of their investments. For example the Predistribution initiative has recognized that the trend of scaled investments into higher risk classes (private equity, venture capital etc.) combined with the greater consolidation of assets under the largest asset managers leads to systemic risks both in the world, such as dramatically deepening inequality, as well as ultimately for investors themselves.

At the same time, pension funds are beginning to feel the heat for the ways in which their direct and indirect investments in housing are contributing to the affordability crisis that affects so many cities globally. Check out an earlier It’s Material piece “Investing People out of Their Homes”, the new Share Canada report “Investors for Affordable Cities”, and Europe-focused report “My home is an asset class”.

“Mainstream” investment and ownership

There will always be trade-offs between state, regional or national priorities and community-level priorities, both when it comes to the need to generate tax revenue from real estate to boost government budgets (the pressure is on in that regard given the economic devastation of the pandemic), and when it comes to infrastructure project investments in ports, transit, energy and so on.

This is where regulatory and planning frameworks, questions of spatial distribution and justice, processes of community-co-creation, and action to mitigate risks and maximize local benefits from the very earliest stages of specific projects throughout their full lifecycle play a crucial role. (Dynamics that my work with the IHRB built environment programme is digging deep into).

{kind=link}

We also need as much transparency as possible over where finance that shapes the places we live is coming from, and how those financial interests are involved in influencing planning and building decisions and policy.

This isn’t simple. Take this diagram of just a subset of urban-related financial flows - climate finance into urban areas:

From: The State of Cities Climate Finance. Among other things the infographic captures quite what an incredibly small proportion of climate finance goes towards adaptation to a changing climate (where returns are lower), than mitigation projects like electrification of transit, and energy efficiency.

Transparency and accountability have a role to play at the level of individual buildings too. Here in NYC where I live, the Real Deal’s comprehensive mapping of the city’s property owners tells an interesting story of who owns the city’s land – with the 10 biggest being the city itself, real estate investment trusts and developers like Vornado, SL Green, Tishman Speyer, Blackstone, Related, Brookfield and RXR, and two universities (Columbia and New York University).

On the housing front, Just Fix NYC does amazing work using open data to “demystify key information for tenants about their homes and landlords and make bureaucratic processes accessible to tenants seeking justice and accountability.”

Speculative development and money laundering

In many ways, real estate investment is more than just that, it is an economic machine. In pretty much any country you can imagine a film in fast-forward mode showing how certain towns and neighborhoods become disinvested while in others gleaming, often empty, luxury towers rise.

Curbing the excesses of speculative real estate and, at the extreme, money laundering, would contribute to the combined goals of reducing inequality by improving the affordability of housing, and reducing the planetary pressure that comes from overbuilding. To loop right back up to how I began this post, last year FACT Coalition published: “The Global is Local – Linking the Fight Against Corruption With Fair Housing in the US”.

A Savills 2016 assessment found that global real estate assets make up nearly 60% of the value of all global assets (of which three quarters is residential, 13% commercial and 12% agricultural). The more we break down what this means in practice, and the ways that it shapes the World we live in today and in the future, the better.

***********

(Here’s me talking about the proximity/connection - distance/extraction line, on a recent webinar together with housing advocate and urban researcher Yahia Shawcat, for the American University in Cairo, around 22 mins in).

Nice Work! I was especially concerned to discover that global real estate assets make up 60% of value of all global assets. I suspect this lies at the heart of real estate expansion, which prevents global targets for climate action and biodiversity loss being met.

This very clear and informative for someone who isn’t immersed in the world of construction and the way it is financed.