Who Owns Cairo?

Transparency and accountability in urban land ownership

{kind=link}

Yahia Shawkat is an urban researcher, and co-founder of the Cairo-based research studio 10 Tooba. Inspired by work in Germany that engaged tenants in tracing the ownership of the buildings that they live in – which often encountered anonymous shell companies at the top of the ownership chain – Yahia wondered what it would look like to map ownership patterns in Cairo. This led to a research project by the Built Environment Observatory, an initiative of 10 Tooba: “Who Owns Cairo?”.

The research team created a methodology for the particular situation of land ownership in Cairo. From the 1990s, the government has increasingly designated land around the edges of Cairo as urban, and either sold it to developers, or has developed it itself. So far approximately half a million acres have been newly designated as urban, a large part of which has been sold. This has led to real estate becoming an increasingly prominent part of Egypt’s GDP, as agriculture has declined: real estate now accounts for 11 percent.

The “Who Owns Cairo” research makes a fundamental point that is applicable to so many countries today, and which prompted me to reach out to Yahia for an interview to learn more about the research:

“Given the size and economic significance of the real estate industry in Egypt, academically it remains understudied, while the general public knows little independent facts about it. A vast range of books and studies have been written about Cairo, its housing, or Egypt’s economics of which land is a sub-section. And while these studies have been invaluable to understand a range of aspects of housing and the real estate market, they are either outdated or have not covered real estate activity itself in-depth…

…[W] hile much is known about agricultural landholdings and ownership, the same is not true for urban landholdings, where thousands of acres of desert as well as coastal land has been privatised over the last three decades…

….urban land ownership, especially for residential purposes, represents the heart of social, economic and political transformations in Egypt, as agricultural land was over the previous centuries.”

The real estate information gap is particularly striking at a time when there is increasing global attention on inequality and a lack of adequate, affordable housing. Who Owns Cairo set out to analyse the Cairo real estate industry’s landholdings and ownership structures in order to start answering the question:

“With vacant unutilised land being a famously abundant resource in Egypt, why is it that affordable housing as a service, and as a right, is still beyond the reach of many?”

In our conversation Yahia also referred to another disconnect, which his work and advocacy seek to bridge: “I was in architecture school and we did urban planning and architecture, but we were never taught, or we never discussed, the links between policy, the real estate market, and housing.”

The research

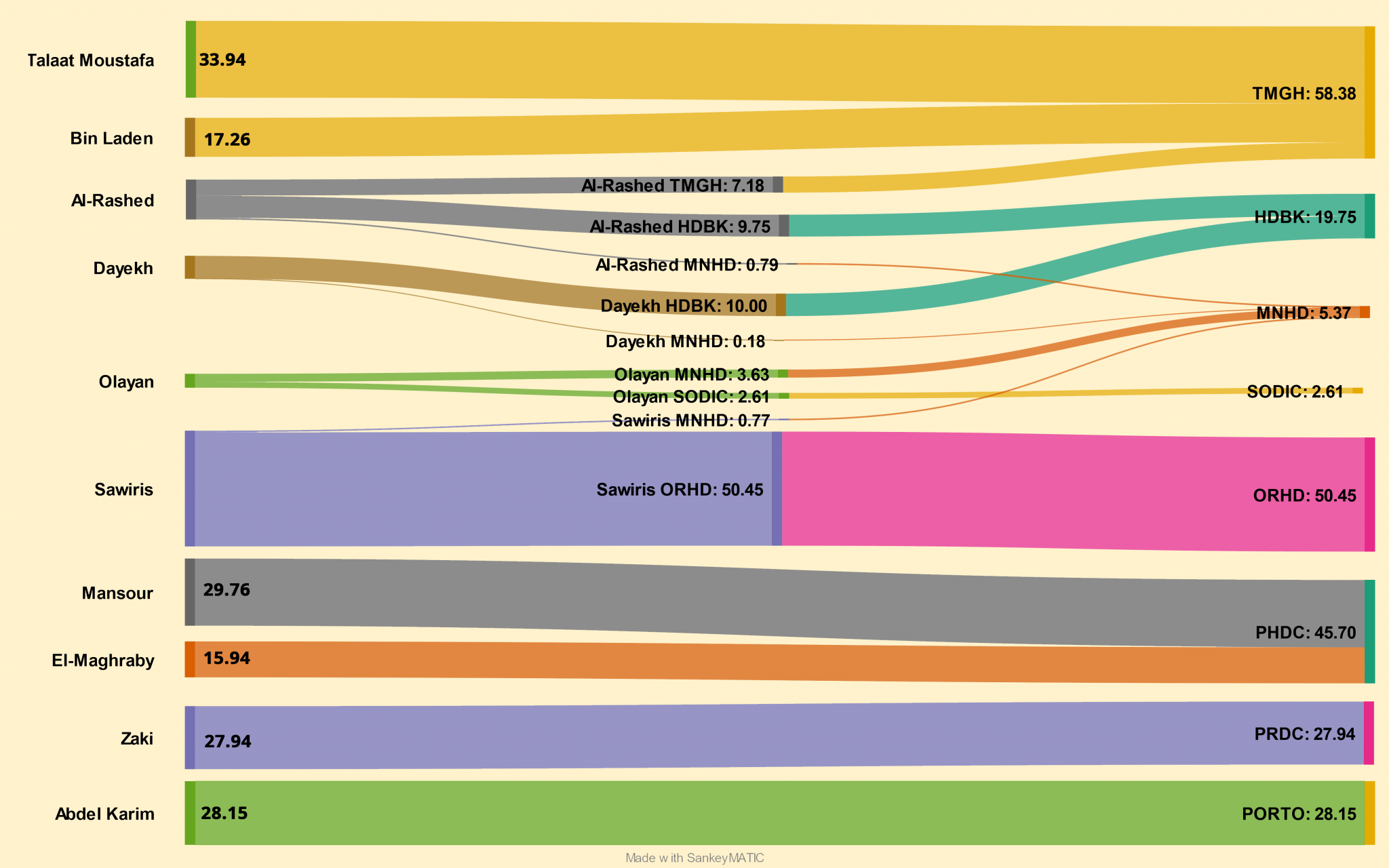

The research process was conducted in three stages: identifying ten case study real estate companies; quantifying their land holdings; and then tracing up to their “beneficial owners”.

Greater Cairo does not have an administrative designation. The research encompassed the urban agglomeration of Cairo and Giza cities, as well as the new cities that have been built, or are still under construction, around them, with significant holdings by large developers.

The first stage was to identify the ten largest listed real estate companies in the region, taking average annual profitability over the past decade as a starting point (full methodology here). The 10 case study companies are:

· Talaat Moustafa Group Holding TMGH.CA

· Palm Hills Development Company PHDC.CA

· Heliopolis Company for Housing and Development HELI.CA

· Six of October Development & Investment SODIC OCDI.CA

· Emaar Misr for Development EMFD.CA

· Madinet Nasr Housing & Development MHHD.CA

· Housing and Development Bank HDBK.CA

· Orascom Development Egypt ORHD.CA

· Pioneers Properties For Urban Development PREDCO PRDC.CA

· Porto Group Holding PORT.CA (Now: Arab Developers Holding ARAB.CA)

The second stage was to identify these companies’ landholdings. Between them they comprise approximately 88% of the total real estate activity across 30 major companies: indicating that the industry is concentrated in these ten, and that they are indicative of the real estate sector as a whole in Cairo.

Third, the study traced direct and indirect owners of the ten case study companies. This combined a tax resident method, so that when multi-level ownership is involved, the last location where a company is registered is identified, and the ultimate beneficiary ownership method, aiming to identify as far as possible the companies’ ultimate owner.

Almost two thirds of Cairo’s case study land of 41,000 acres was traced to four identifiable investor groups: private individuals/families, states, private companies, and listed funds. The remaining 35% is held by thousands of smallholders.

1. Private families

Ninety-three private individuals and families hold 36% of the case study land (and 85% of this group’s landholdings is owned by just seven investors, with controlling stakes in five of the ten listed real estate companies).

2. State owned enterprises

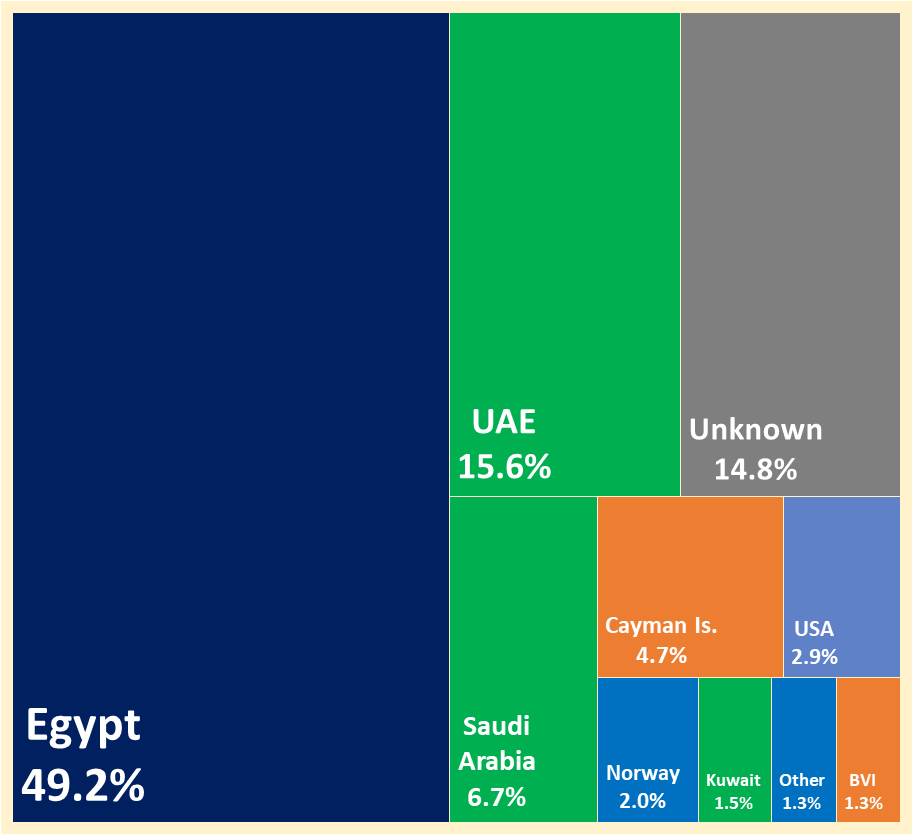

Egyptian and foreign state owned enterprises (SOEs) own 25% of the case study land. The Government of Egypt and the Government of the United Arab Emirates each control two of the case study companies, while Norway and Kuwait have minority holdings across the companies.

As Yahia says, this “brings into play the question of politicizing housing. Because this kind of high level investment by other states does not come just purely as an investment opportunity, but also has the power…power and control affect policy.” In recent years, the sovereign wealth funds of Gulf states in particular have grown significantly in scale and reach globally.

As the research also notes, the role of the SOEs prompts questions “about the social function of state enterprise, where the majority of projects analysed in this study cater to upper middle income and upper income buyers.”

3 and 4. Private companies – unlisted and listed

In third place are Vanguard Group, Inc., with smallholdings in seven of the ten case study companies, and the BIG Investment Group Ltd, a special investment fund owning a controlling share in one of the case study companies. The final group is large transnational corporations listed on stock exchanges, which own 1% of the case study land: BlackRock, HSBC and Russell Investment Management.

Regarding owners’ nationality, using the tax residency method, the ownership breaks down as follows:

Explore all of the findings here.

The findings tell a story of consolidation, at various levels. One, as Yahia describes, is the significance of controlling investors, and therefore a note for future research that it makes sense to focus as much as possible on controlling investors: “We tracked almost a hundred investors. But it’s really maybe only 10 or 15 or these that call the shots”. Another is the scale of the landholdings of the individual companies, meaning that while you might expect one owner to aim to have a stake in several companies, in fact “they don’t need that because some companies have extraordinarily large landholdings to begin with…[so] the government has facilitated a consolidation, concentration of ownership.”

This concentration of the formal real estate market also has implications for the dynamics between the formal market and the informal housing sector, including in the area of building materials.

“From one side there’s a big divide between the informal market and the formal market. But at the end of the day, they're completely related because they buy materials from the same producers. Other than land, the resources are the same: workers’ labour and building materials are affected by the demand of these two markets. Yet given the economies of scale, big developers can buy their materials much cheaper than informal developers.”

One of Yahia’s takeaways and recommendations of the research, is that “even though we started out looking at the private sector – and there may be cause for concern from certain developers – a lot of this inequity should be addressed by restructuring how the government deals in land.” This, he recommends, would include breaking up the urban development authority into separate entities, to reduce conflicts of interest and ensure oversight while maintaining some state role in developing housing.

Linking this back to the goals of the research, the findings begin to reveal dynamics behind the housing affordability challenges and contradictions that Cairo and other cities face.

“Ultimately for Egyptian cities and many other cities now, there is this internationalization of the housing market, which pits tenants and buyers against international money. So your buying power or your renting power is automatically reduced because you are competing against people – or more and more against institutions – that have much more buying power than you.”