BlackRock buys Global Infrastructure Partners

Setting priorities for the future of infrastructure

This month the World’s largest asset manager BlackRock acquired Global Infrastructure Partners for $12.5 billion in cash and stock. The move is a clear sign of the expansion of private investment in infrastructure within mainstream markets. BlackRock CEO Larry Fink declared that the global economy is on the cusp of an “infrastructure revolution”, due to decarbonization, digitization and deglobalization.

As BlackRocks’s press release puts it:

“A number of long-term structural trends support an acceleration in infrastructure investment. These include increasing global demand for upgraded digital infrastructure like fiber broadband, cell towers and data centers; renewed investment in logistical hubs such as airports, railroads and shipping ports as supply chains are rewired; and a movement toward decarbonization and energy security in many parts of the world.”

In fact, the shift towards infrastructure as an investable asset class is not new. It gathered steam through the 1990s as governments began turning to private investment, and was further accelerated from 2015, when international financial institutions like the World Bank and IMF advanced a “billions to trillions” agenda, calling for private finance to help meet the 2030 Sustainable Development Goals.

Still, the renewed focus now means it is an opportune moment to think about the ways that private investment into infrastructure brings risks to people, as well as opportunity – and to call for collaborative and longer-term thinking that gets investments right.

Structures that are geared to making as much money as possible for investors in the short term, can bake in risks to people and deepen existing inequalities. For example, through increased tolls for transit use, increased costs of water, and decreased investment in maintenance over time, while paying private fund managers high fees.

The Financial Times’ has reported for example, on the track record of the World’s largest infrastructure asset manager, the Australian firm Macquarie. It looked in particular at its acquisitions of water utilities in the UK, where its model of buying essential public services, taking on high levels of debt and paying high returns out to shareholders has seen increased water leaks and discharges of sewage into the oceans. (Just four days ago, Macquarie announced it has raised over €8 billion for a new European infrastructure investment fund).

On the public sector side, there is no shortage of mismanagement, corruption, and dire lack of investment in and maintenance of infrastructure of course. So the key is how can public and private goals become better aligned: to create and maintain much-needed infrastructure in ways that serve its core purpose, take the most vulnerable users’ rights and needs into account from the outset, support a shift to low-carbon economies, and generate stable returns.

The status-quo isn’t working, so the case should be easy to make: only 8.5 percent of major infrastructure projects are delivered on time and on budget. The Office of the High Commissioner for Human Rights (OHCHR’s) key report “The Other Infrastructure Gap: Sustainability” says:

“Private finance can play a much greater role in infrastructure financing, but it is not a panacea. Infrastructure finance is a shared responsibility of public and private actors. Public authorities should discharge their public governance responsibilities, and investors should accept that they are custodians of a public asset and not mere private recipients of cash flow.”

This custodianship responsibility is being increasingly recognized by some infrastructure investors, which is a welcome development.

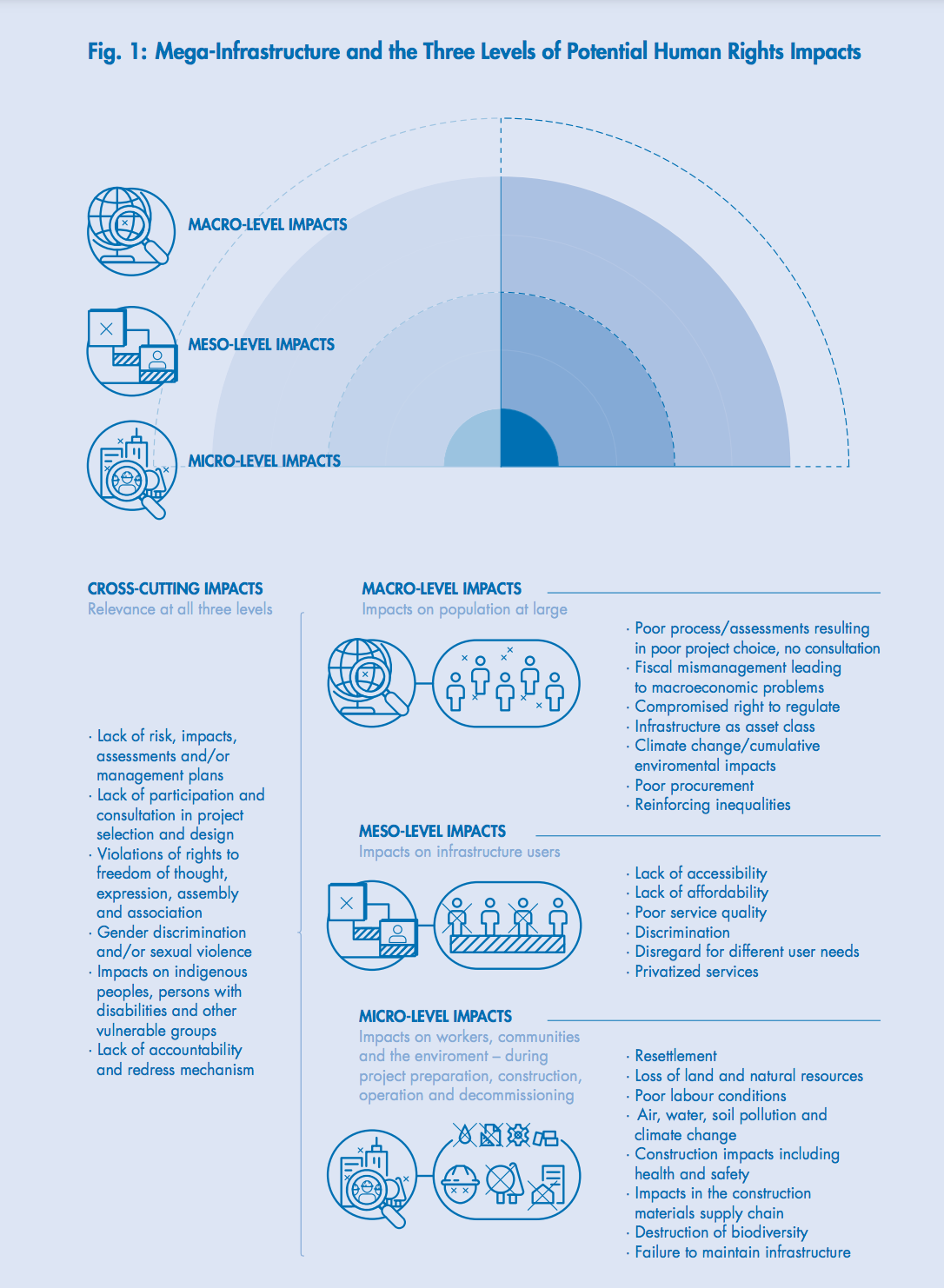

The OHCHR report usefully maps out three levels at which social and environmental risks need managing, as well as the roles and responsibilities for doing so:

Micro-level: The direct impacts on local communities and workers when land is acquired for a project, and construction takes place

Meso-level: The level of access to and affordability of infrastructure services such as water, energy, and transport, for the users of those services

Macro-level: The impacts for wider populations and tax payers, for example the risk that inefficient, incomplete or badly managed projects can waste public resources and lead to “fiscal burdens, over-indebtedness, austerity and withdrawal of public services.”

Much of the drive for private investment into infrastructure – including one of BlackRock’s reasons for wanting to expand in this space – is coming from pension funds and from Sovereign Wealth Funds, which respectively have retirees’ and their countries’ future generations baked into their purpose. (More on Sovereign Wealth Funds in a future newsletter: they now account for almost 40% of total assets among the World’s 100 largest asset owners).

The kind of infrastructure we build has a material impact on the environment and on people, now and well into the future. It’s time to continue driving a shift in perspective, from the quick buck a project can make for a few, to partnerships on wider and longer-term value.